Real Interest Rates:

A “Perfect Storm” for Fixed Income Investors

Jerry Paul, CFA – Senior VP of Fixed Income

December 14, 2020

Driven largely by the lack of real interest rates, bond investors are faced with a “Perfect Storm,” resulting in historically low interest rates with real interest rates explaining the largest part of the problem. This paper will discuss this environment.

In the fall of 2017 ICON published a white paper called: “Real Interest Rates: The Mystery of Low to Non-Existent Real Rates”. I recommend reading that paper in conjunction with this updated version as it details some of the technical and theoretical reasons for low or non-existent real interest rates. These include the decline in the equilibrium real interest rate, the safe assets shortage conundrum, the global savings glut, and the effects of Federal Reserve holdings on interest rates. Several of these are even greater issues today than in 2017.

Our 2017 paper previously made several critical observations:

- Real interest rates averaged .70% from 2008-2017 vs. 2.80% from 1970-2007

- It is real interest rates that represent improved purchasing power and a higher standard of living for those receiving interest income from investments.

- Our conclusion is that investors should be cautious in their expectations for higher real rates in the near future.

It turns out I was too optimistic – real interest rates have fallen even further and are now negative! When we published the 2017 paper the UST 10-year was yielding 2.40%. In 2020 it yields .85%, up from a recent low of .52%.

Inflation has continued in the range of 1.25%-1.75%, as measured by the Fed’s preferred metric of Personal Consumption Expenditures (PCE), and in September it was 1.40%. Accordingly, real interest rates are currently -.55% after reaching a low point of -1.12% in March!

Also to consider is, at the time we were putting together “The Mystery of Low to Non-Existent Real Rates” in 2017 the Federal Reserve was beginning the process of reducing its balance sheet, which was expected to put upward pressure on interest rates. As a result of the economic crisis precipitated by COVID -19 there has been a total reversal and expansion of asset purchases beyond the Fed’s previous level. In addition, Investment Grade and High Yield bonds were included in the Fed’s asset acquisition for the first time. Currently the Federal Reserve balance sheet has grown to $7.1 trillion and many experts expect it to exceed $10 trillion!

When I look at all these factors I again conclude there is no reason to expect real interest rates to return to historical levels and they may remain negative for some time given current events.

Recent Federal Reserve statements suggest they will hold interest rates lower for a longer period than previously expected. When this is combined with negative real interest rates, fixed income investors will likely be challenged to realize the current income they may have expected or require for their lifestyle.

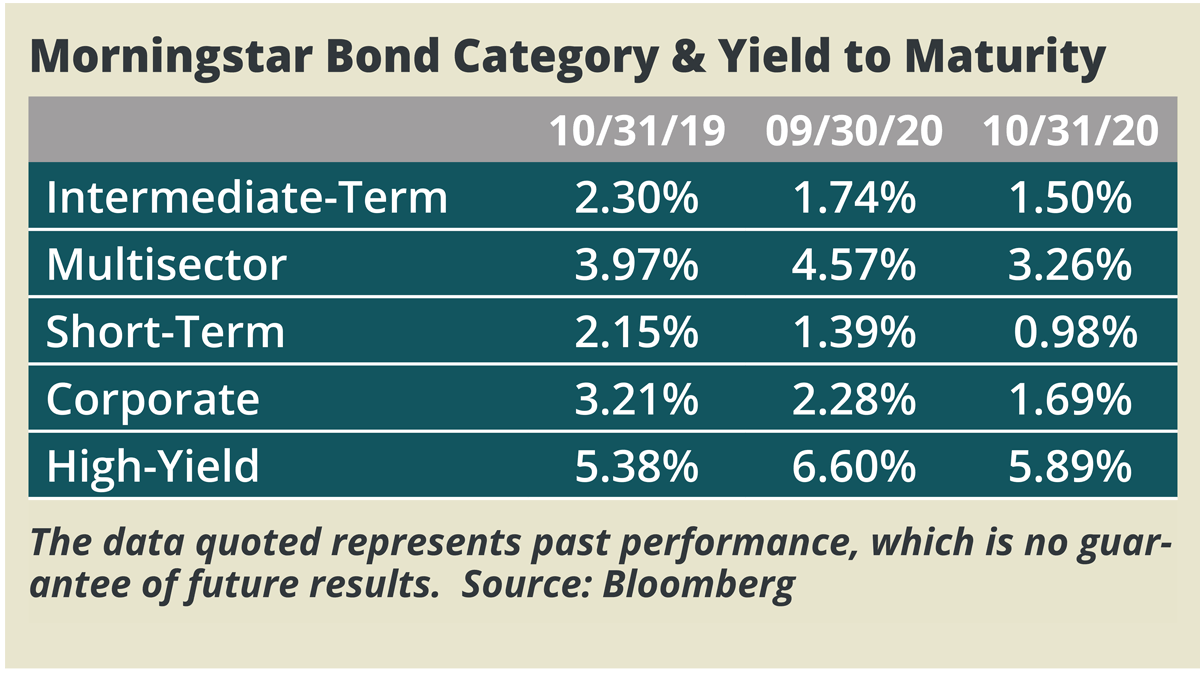

Fixed income mutual fund yields reflect the decline in real interest rates over the past 12 months. The decline in fixed income mutual fund dividends has been dramatic over this time (as large as 20+ %), but has recently accelerated as corporate refinancing has increased, resulting in higher coupon bonds being called away. This may worsen as corporate yield-spreads have tightened significantly in the past two months enabling further refinancing of high coupons. This can be seen in the Yield to Maturity (YTM) of several of the Morningstar Fixed Income Categories.

It would seem to only be a matter of time, possibly less than 3-6 months, before we see some bond mutual fund yields declining below 1% and 2% depending on their category!

As we can see, it appears interest rates are facing a “perfect storm,” resulting in historically low interest rates with real interest rates explaining the largest part of the problem. Real interest rates are as much as 250 basis points below normal, and restoration of these would put the UST 10-year over 3%. Corporate yield spreads are low to normal, but this may be inadequate compensation for investors in the current economic environment where uncertainty and the risk of defaults is higher than normal. The Federal Reserve also has a policy of keeping interest rates lower for longer periods, significantly increasing its balance sheet through UST and MBS purchases. Prior to Covid-19 the UST 10-Year was trading in the 1.60%-1.90% range. Even at the high end we would still only have a real interest rate of 50bps!

In Conclusion:

- It is important for advisers and investors to understand real interest rates repre- sent improved purchasing power and a higher standard of living for those receiving interest-income from investments.

- We continue to believe investors should be cautious in their expectations for higher real rates in the near future. In fact, we are likely in an extended period of below-average real interest rates.

- Bond fund investors may not be able to avoid the impact of low to negative real interest rates. Investors may need to identify bond funds that can minimize the impact.

- We believe we are in a “perfect storm” resulting in historically low interest rates with real interest rates explaining the largest part of the problem.

Jerry Paul, CFA, is Senior Vice President of Fixed Income and serves as Portfolio Manager of the ICON Bond Fund and Co-Portfolio Manager of the ICON Equity Income Fund.

The data quoted represents past performance, which is no guarantee of future results. Opinions and forecasts regarding sectors, industries, companies, countries and/or themes, and portfolio composition and holdings, are all subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security, industry, or sector

As an investment professional you are responsible for knowing your clients’ needs, goals, and tolerance for risk and advising your clients accordingly.

There are risks involved with mutual fund investing, including the risk of loss of principal. There is no assurance that the investment process will consistently lead to successful results. Investing in fixed income securities such as bonds involves interest rate risk. When interest rates rise, the value of fixed income securities generally decreases. High-yield bonds involve a greater risk of default and price volatility than U.S. Government and other higher-quality bonds. An actively managed investment product does not guarantee better returns or performance than any other kind of investment.

Real Interest Rate is defined as an interest rate that has been adjusted to remove the effects of inflation to reflect the real cost of funds to the borrower and the real yield to the lender or to an investor. The real interest rate of an investment is calculated as the amount by which the nominal interest rate is higher than the inflation rate

Morningstar Intermediate-term Bond portfolios invest primarily in corporate and other investment-grade U.S. fixed-income issues and typically have durations of 3.5 to 6.0 years. These portfolios are less sensitive to interest rates, and therefore less volatile, than portfolios that have longer durations. Morningstar calculates monthly breakpoints using the effective duration of the Morningstar Core Bond Index in determining duration assignment. Intermediate-term is defined as 75% to 125% of the three-year average effective duration of the MCBI. Multisector Bond portfolios seek income by diversifying their assets among several fixed-income sectors, usually U.S. government obligations, U.S. corporate bonds, foreign bonds, and high-yield U.S. debt securities. These portfolios typically hold 35% to 65% of bond assets in securities that are not rated or are rated by a major agency such as Standard & Poor’s or Moody’s at the level of BB (considered speculative for taxable bonds) and below. Short-term Bond portfolios invest primarily in corporate and other investment-grade U.S. fixed income issues and typically have durations of 1.0 to 3.5 years. These portfolios are attractive to fairly conservative investors, because they are less sensitive to interest rates than portfolios with longer durations. Morningstar calculates monthly breakpoints using the effective duration of the Morningstar Core Bond Index in determining duration assignment. Short-term is defined as 25% to 75% of the three-year average effective duration of the MCBI. Corporate Bond portfolios concentrate on bonds issued by corporations. These tend to have more credit risk than government or agency-backed bonds. These portfolios hold more than 65% of their assets in corporate bonds, hold less than 40% of their assets in foreign bonds, less than 35% in high yield bonds, and have an effective duration of more than 75% of the Morningstar Core Bond Index. High-yield bond portfolios concentrate on lower-quality bonds, which are riskier than those of higher-quality companies. These portfolios generally offer higher yields than other types of portfolios, but they are also more vulnerable to economic and credit risk. These portfolios primarily invest in U.S. high-income debt securities where at least 65% or more of bond assets are not rated or are rated by a major agency such as Standard & Poor’s or Moody’s at the level of BB (considered speculative for taxable bonds) and below. Total returns for the unmanaged indexes include the reinvestment of dividends and capital gain distributions but do not reflect the costs of managing a mutual fund. The Fund’s composition may differ significantly from the index. Individuals cannot invest directly in an index.

The 10-year yield is the benchmark 10-year yield to maturity reflected by the current issue 10 year U.S. Treasury note. Yield to maturity (YTM) is the total return anticipated on a bond if the bond is held until it matures, expressed as an annual rate.

Data Sources: Bloomberg

Please visit ICON online at www.InvestwithICON.com or call 1-800-828-4881 for the most recent copy of ICON’s Form ADV, Part 2.

© 2020 ICON AdvisersSM All Rights Reserved.