It’s Money Supply not Interest Rates

Craig Callahan, DBA

September 22, 2019

There are two popular views regarding the economy and monetary policy. One is that the U.S. economy is on the edge of tipping into recession. The second is that with interest rates so low, the Federal Reserve (FED) does not have the ability to stimulate the economy. We strongly disagree with both of those positions.

The problem with those two positions, particularly the second, is that they are interest rate based. They assume there is a direct relationship between the Federal Funds rate, which the Federal Reserve sets, and the economy. In other words, the rate goes up, the economy slows. The rate goes down, the economy speeds ups. The reason observers gravitate toward this view is that the interest rate change is all they can see and touch and humans like to simplify things to one-on-one, cause and effect relationships. A causes B, and C causes D; case closed. As convenient as that is, the economic world does not work that way. Running a simple regression on the two factors produces no significant relationship and produces a correlation coefficient close to zero, meaning no statistical relationship between Fed Funds and GDP.

What is going on with monetary policy? When the FED lowers its target for Fed Funds, it buys T-Bills from banks, and pays for them by adding reserves to the bank’s account at the FED. With increased reserves, banks can make more loans, which in turn creates money. There is a direct relationship between the rate of growth of the money supply, M1, and economic growth. The monetarists have the equation MV =PQ, where M is the money supply, V is the velocity of money, P is the prices of all goods & services and Q is the quantity of goods & services. If M is increased and V stays constant, total spending, as measured by Price times Quantity on the right has to increase. It is not the lower interest rate that stimulates the economy, it is the increase in M1 but since observers can’t see, touch or get their arms around the M1 increase they default to the interest rate based model.

Even with low interest rates the FED has three tools which can be effective to increase the money supply and stimulate the economy. All three inject reserves into banks which allows them to make more loans which grows M1. First, as described above, the FED can lower the Fed Funds target and perform Open Market Operations. It buys T-Bills from banks and pays for them by adding to the bank’s reserves. Then banks can make more loans. Second, the FED could lower the rate on the Discount Window. Day to day, banks borrow reserves from each other which does not increase reserves over the entire banking system, but when the FED lowers the rate at the Discount Window, banks borrow reserves from the FED which injects reserves into the system. Again, more reserves means more loans as there is a fixed ratio of loans per dollar of reserves on each bank’s balance sheet. Third, the FED can lower the Reserve Requirement. Immediately banks can put more loans on the books per dollar of reserves that they hold. All three tools result in more loans, which creates money; more money, M1, more economic growth. It isn’t the change in interest rates that promotes growth, it is the increase in the money supply and the FED has the ability to do that even in a low interest rate environment.

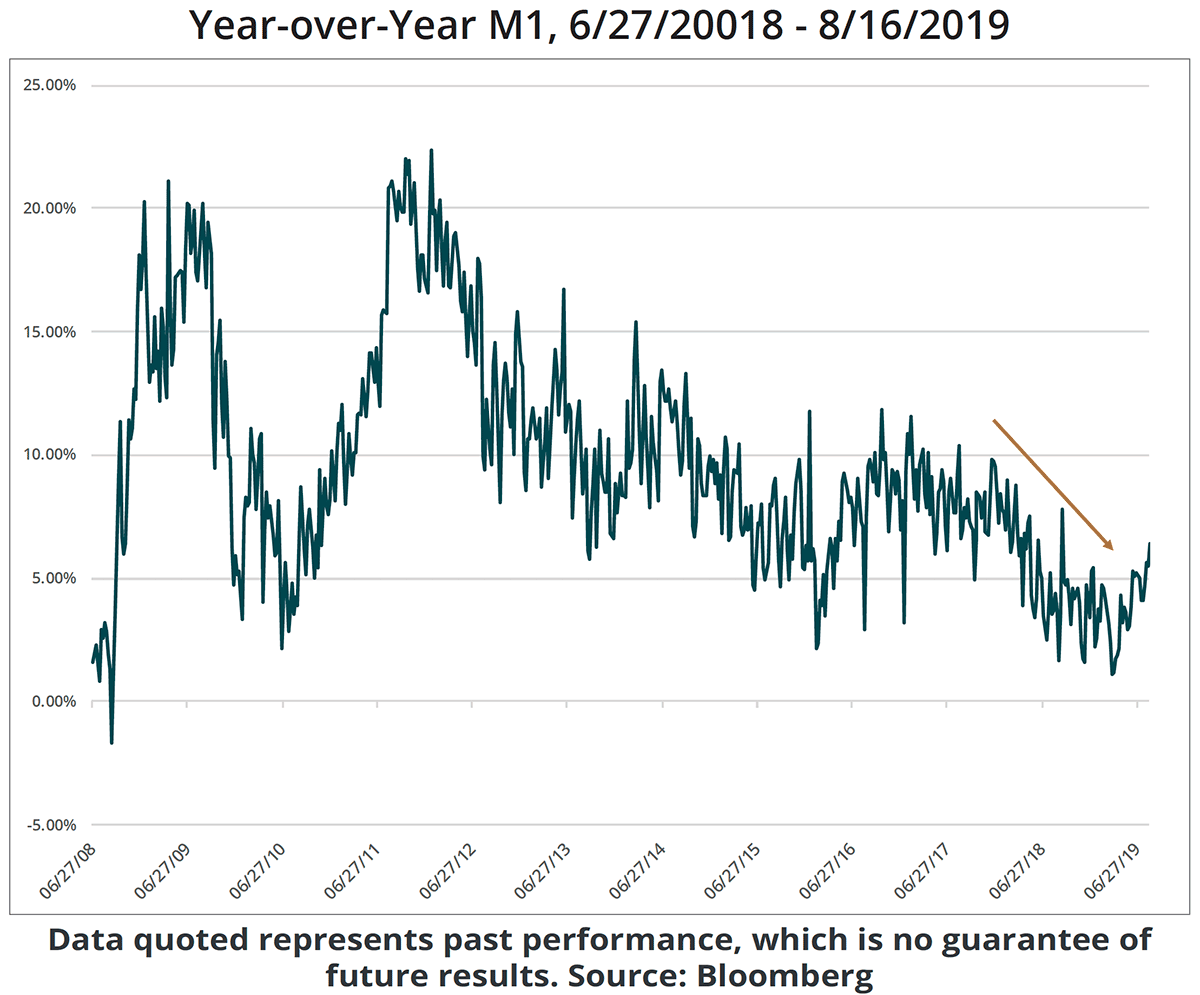

As for on the edge of tipping into recession, the graph shows year-over-year, or 52 week rate of change for M1 back to June 27, 2008.

In 2008, the FED got the money supply growing 20% year-over-year trying to jolt the economy out of the great recession. Incorrectly concerned about inflation, it slowed growth back down to below 5%. It then realized the economy had not gained momentum and increased year over year growth in M1 back up to 20%. Since that peak, the rate of growth of M1 has been generally slowing, especially in 2017 and 2018 (highlighted by the arrow) when the FED raised its Fed Funds target. To accomplish that, it sold T-bills to banks and drained reserves, which slowed lending and the creation of money. By late March of 2019, Y-O-Y growth in M1 was down to 1.1%. Realizing it went too far, the FED apparently has been buying T-bills, injecting reserves and stimulating loan and money supply growth again. For data released August 16, 2019, Y-O-Y growth in M1 is back up to 6.4%, slightly above its historic average.

It is our opinion that with M1 growing at recent levels, a recession is highly unlikely. There are some clouds like tariffs with China and some slowing in industrial investment, but we will put our money, so to speak, on M1. Relying on M1 is not a new position for us. In our November 2008, Portfolio Update to investors we wrote, “The increase in M1 since last May (2008) suggests to us that banks are lending again and thereby creating M1. Subscribing to the monetarist view, we would expect that M1 growth to fuel the economy and spark a recovery in a few quarters.” The stock market began its multi-year bull four months later, and the economy had positive quarterly GDP growth three quarters later, third quarter 2009. In late 2008 and early 2009, we used the phrase ”the cavalry is on the way” to describe the potential stimulus from M1. Although not the 20% we saw back then, 6.4% is adequate to prevent a recession.

Dr. Craig Callahan is the Founder and President of ICON, and is chairman of the ICON Investment Committee. He is also Portfolio Manager for the ICON Fund and the ICON Opportunites and Long/Short Funds and Co-Portfolio Manager of the ICON Risk-Managed Balance Fund.

The data quoted represents past performance, which is no guarantee of future results.

Opinions and forecasts are subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security, industry, or sector.

Investing in securities involves risks, including the risk that you can lose the value of your investment. There is no assurance that the investment process will consistently lead to successful results.

M1 is one measure of the money supply that includes all coins, currency held by the public, traveler’s checks, checking account balances, NOW accounts, automatic transfer service accounts, and balances in credit unions. Gross Domestic Product (GDP) is the total value of goods and services produced in the national economy in a given year. It is the primary indicator of economic growth. A Treasury bill (T-Bill) is a short-term debt obligation backed by the Treasury Dept. of the U.S. government with a maturity of less than one year.

Source: Bloomberg

Please visit ICON online at www.iconadvisers.com or call 1-800-828-4881 for the most recent copy of ICON’s Form ADV, Part 2.