Craig Callahan, DBA

Founder & President

- Portfolio Manager of the ICON Funds

- Created ICON’s proprietary valuation model

- Founded ICON in 1986

Why Claims that “The Market Was Expensive” Were Wrong

Dr. Craig Callahan, ICON Advisers – Founder & President

October 13, 2020

During the rally off the market low on March 23, 2020, many skeptics and doubters claimed stocks are too expensive and that the rally is irrational. As an example, on May 13, 2020 CNBC Markets published an article stating, “Billionaire hedge fund investor David Tepper told CNBC on Wednesday the stock market is one of the most overpriced he’s ever seen, only behind 1999. His comments sent stocks to a session low.” Mr. Tepper did not mention the basis for his claim, but later the article stated, “The S&P 500’s forward price-earnings ratio based on estimates for the next 12 months has ballooned to above 20, a level not seen since 2002.”1

The use of the P/E ratio for the S&P 500 Index is a popular tool for gauging the valuation level of the broad market. Unfortunately, we believe those analysts using P/E have been wrong here in 2020 just as they were incorrect during the early stages of the great 11-year bull market, which began in March 2009 and ended February 2020. By the end of February 2009, just before the market bottom of March 9, the P/E on the S&P 500 was 10.95. By the end of November the ratio had soared to 22.08, due to stock prices increasing and earnings dropping. There were claims that stocks were expensive and over-priced, but in looking back we know those claims were wrong and the bull market continued another ten-plus years. Let’s look at why P/E ratios are leading some analysts in the wrong direction.

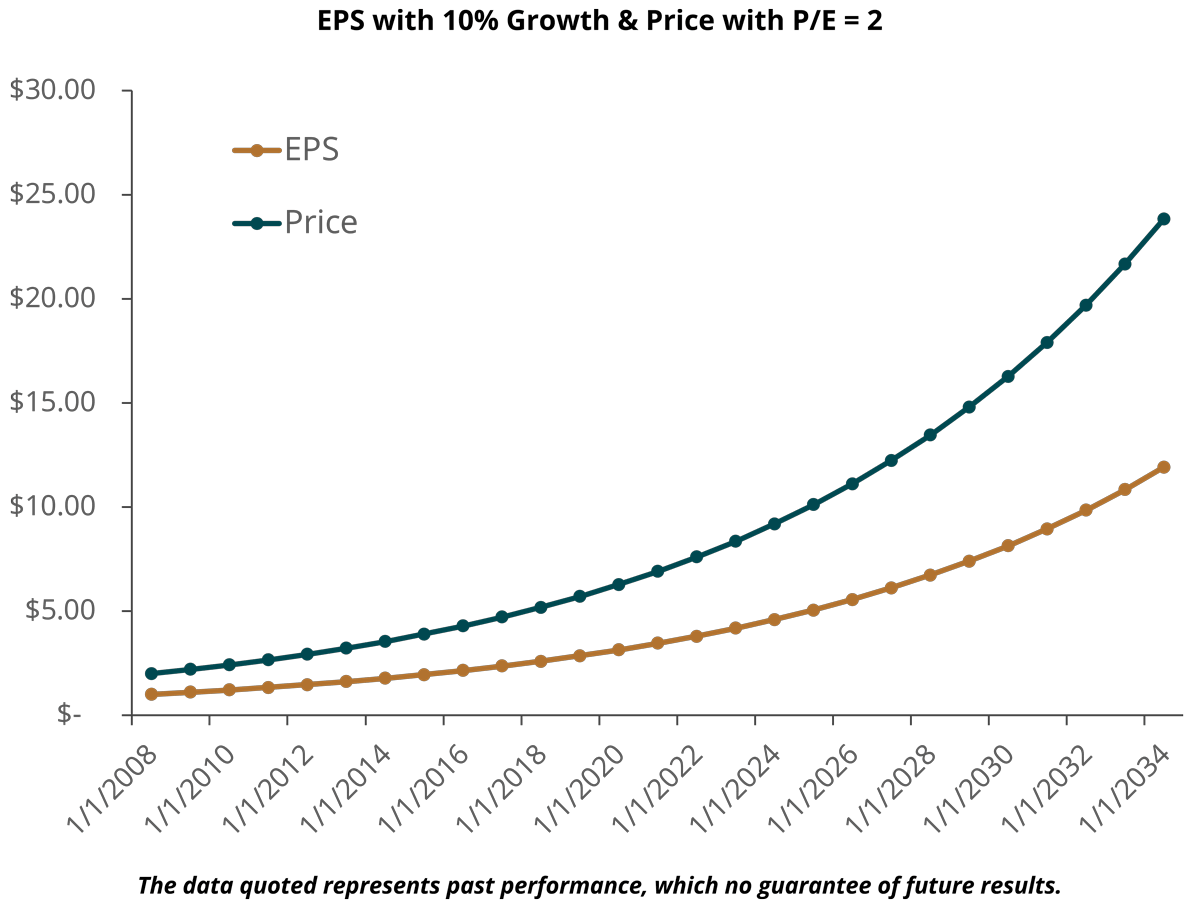

The blue line of the graph below shows earnings per share (EPS) for a company growing at a steady 10% per year from a base of $1.00. The orange line shows what the price would be if investors thought a P/E of 2 was proper all the time. Admittedly a P/E of 2 is extremely low, but this allows price and earnings to be compared proportionately without distorting results or altering the overall concept.

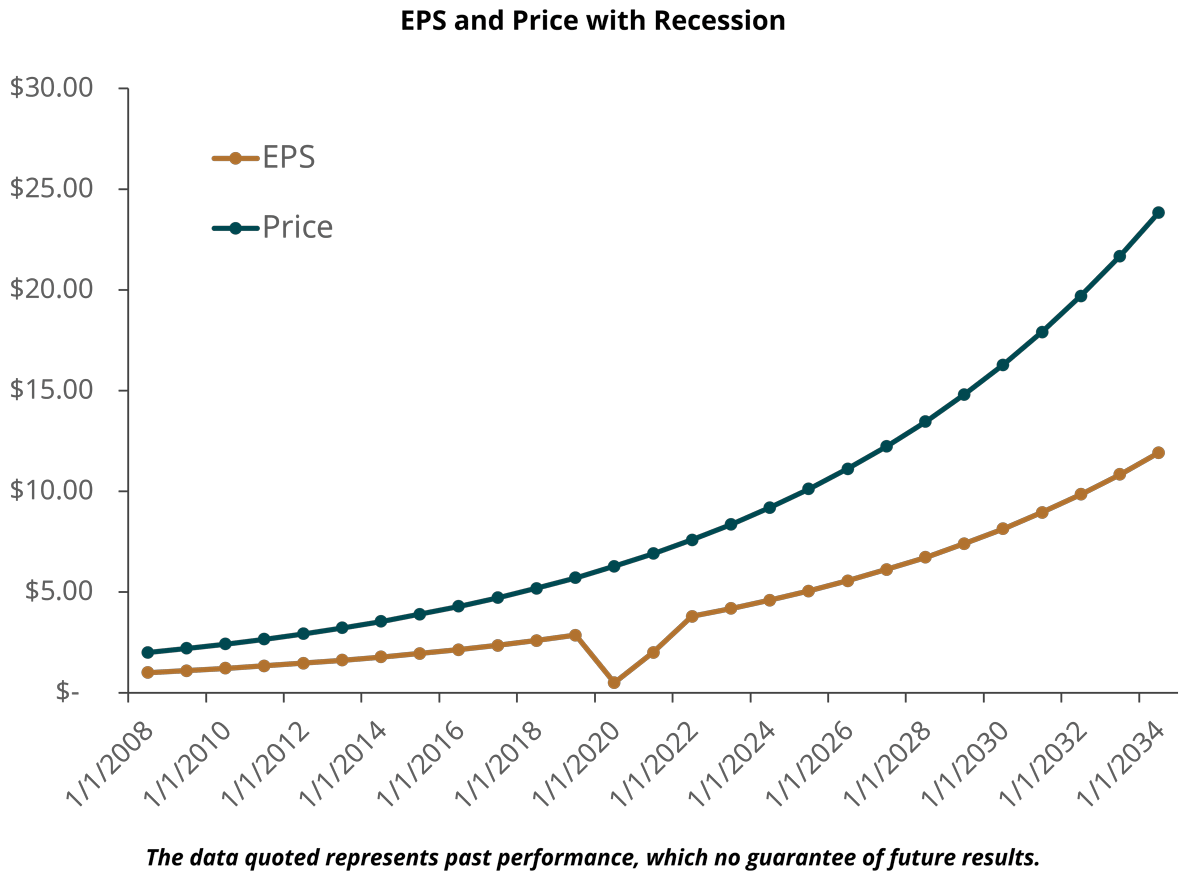

What happens if there is a virus pandemic and a self-imposed recession in 2020? Hypothetically let’s say this company’s earnings are only $.50 in 2020 and $2.00 in 2021 instead of the stock prices of $6.28 and $6.90, respectively, that they would have been without the self-imposed recession. Let’s also say the stock price drops sharply at first when investors realize there will be a recession but that there would be a quick recovery to where the price would have been absent the recession. This set of events and circumstances is shown in the second graph, note the $.50 and $2.00 EPS in 2020 and 2021.

With earnings of $.50 and a price back to $6.28, the P/E ratio would be 12.6 and would appear astronomical to investors thinking a P/E of 2 is proper. The next year, with earnings recovering a bit to $2.00 and price at $6.90, the P/E would be 3.5, continuing to convey that the stock is expensive. A common practice among some users of P/E is to take current price but divide by EPS one year ahead, as CNBC did in the May 13 article quoted above. In this case, the 2020 price of $6.28 divided by 2021 earnings of $2.00 gives a “forward” P/E of 3.1, again suggesting the stock is expensive to those investors thinking a P/E of 2 is proper.

The use of the simplistic but easy to use P/E has many deficiencies. This is just one of them. Fair value for a stock or any asset is the present value of future earnings. Given the expectation that earnings will recover and grow at 10% per year, the stock in this example was worth $6.28 in 2020 and the notion that it was expensive because it was priced at 12.6 times earnings is, to ICON, ridiculous.

In 2020 there are some companies on a growth path that was not affected by the virus and recession. At the other end, there were companies whose earnings were severely impacted by the recession and they do not have good prospects for recovery. For the majority of companies, however, their earnings look like the second graph; down initially and then recovering to their previous potential path. Based on intrinsic value being the present (or discounted) value of their future earnings, the rally of 2020 is very sensible. Investors are pricing in the future, not the present.

The data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate and shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the data quoted. Please call 1-800-828-4881 or visit www.InvestwithICON.com for performance results current to the most recent month-end. Results are net of fees and calculated in U.S. dollars.

Opinions and forecasts regarding industries, companies and/or themes and portfolio composition and holdings are all subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security, industry or sector.

Investing in securities involves risks. There is no assurance that the investment process will consistently lead to successful results.

ICON’s value-based investing model is an analytical, quantitative approach to investing that employs various factors, including projected earnings growth estimates and bond yields, in an effort to determine whether securities are over- or underpriced relative to ICON’s estimates of their intrinsic value. ICON’s value approach involves forward-looking statements and assumptions based on judgments and projections that are neither predictive nor guarantees of future results. Value readings are contingent on several variables including, without limitation, earnings, growth estimates, interest rates and overall market conditions. Although valuation readings serve as guidelines for our investment decisions, we retain the discretion to buy and sell securities that fall beyond these guidelines as needed. Value investing involves risks and uncertainties and does not guarantee better performance or lower costs than other investment methodologies.

1 Li, Y. (2020, May 13), David Tepper says this is the second-most overvalued stock market he’s ever seen, behind only ’99. CNBC Markets, Retrieved from https://www.cnbc.com/2020/05/13/david-tepper-says-this-is-the-second-most-overvalued-stock-market-hes-ever-seen-behind-only-99.html

The unmanaged Standard & Poor’s (S&P) 500 Index is a market value-weighted index of large-cap common stocks considered representative of the broad market. Total return for the unmanaged index includes the reinvestment of dividends and capital gain distributions but do not reflect deductions for commissions, management fees, and expenses. Individuals cannot invest directly in an index.

Price/Earnings Ratio (P/E) is the price of a stock divided by its earnings per share. Earnings Per Share (EPS): Earnings from ongoing operations; earnings per share equals total earnings divided by the number of shares outstanding.

Please visit ICON online at InvestWithICON.com or call 1-800-828-4881 for the most recent copy of ICON’s Form ADV, Part 2.

ICON Blogs

![]()

ICON Advisers, Inc.

8480 E Orchard Road, Suite 1200

Greenwood Village, CO 80111